Financing land or acreage is very different from buying a standard suburban home. Many buyers quickly discover that not all mortgage programs work well for rural properties, especially if the plan includes multiple acres, a modular home, or off-grid living. Two of the most common options buyers consider are conventional vs FHA loans, but which is better for buying acreage?

The answer depends on your financial profile, build plans, and long-term goals. In this article we explore the differences of down payments and interest rates to appraisals and building flexibility. Before buying land check out our Top 3 Things You Need to Know Before Buying Rural Land article.

What Is an FHA Loan?

An FHA loan is a mortgage backed by the Federal Housing Administration, a government agency. It’s designed to help buyers with lower credit scores or smaller down payments qualify for home financing. Many people think it is for first time buyers but it is not. But itt can only be used once every 7 years in most cases.

What Is a Conventional Loan?

A conventional loan is not backed by the government. It follows guidelines set by private lenders, like Envoy, and typically requires stronger credit and higher down payments, but offers more flexibility long term.

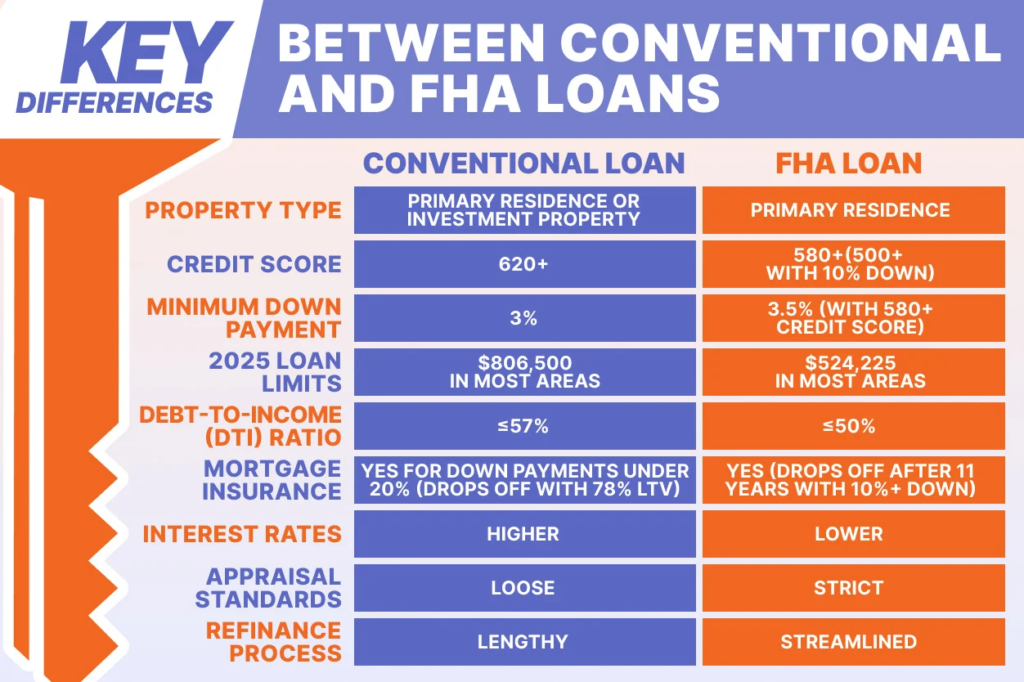

Down Payments: How Much Cash Do You Need?

One of the biggest differences between conventional vs FHA loans is the down payment requirement.

- FHA loans allow down payments as low as 3.5% for buyers with credit scores of 580 or higher. This makes FHA financing attractive for buyers with limited cash or those prioritizing liquidity for land improvements.

- Conventional loans typically require a down payment of 5–20%, depending on the credit, lender, and property type. When acreage is involved, some lenders may require higher down payments due to perceived risk.

For buyers trying to preserve savings for wells, septic systems, fencing, or utilities, FHA loans can offer more flexibility upfront. If you’re interested in no-down payment check out the USDA Rural Development Loan, which may be an even better option since it was created for developing rural land.

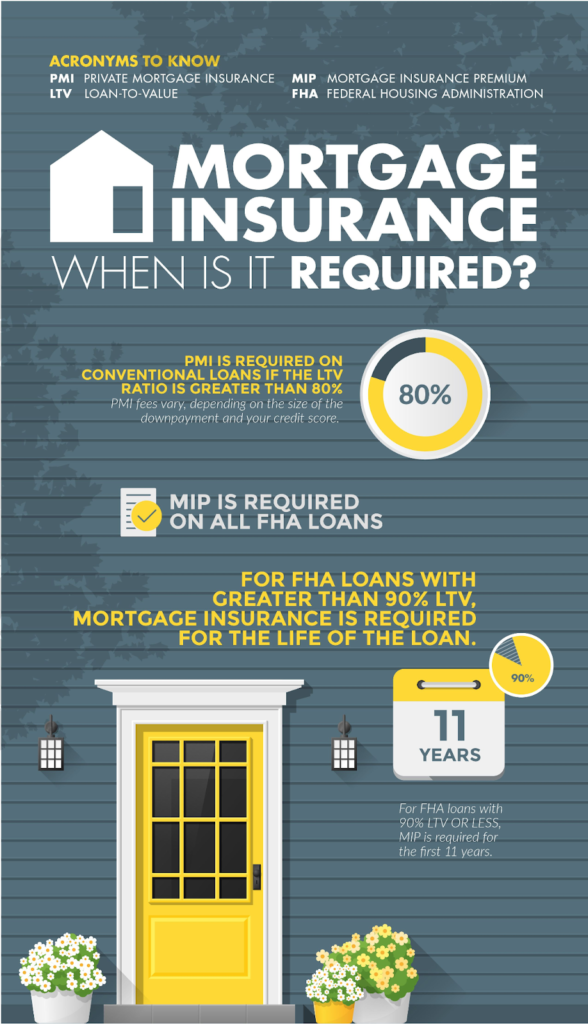

Interest Rates and Mortgage Insurance: Conventional vs FHA Loans

Interest rates for both conventional vs FHA loan types can be competitive, but there are key differences:

- FHA loans often offer slightly lower interest rates, especially for borrowers with average credit.

- Conventional loans may offer better long-term savings for buyers with strong credit because private mortgage insurance (PMI) can be removed, while FHA mortgage insurance typically lasts the life of the loan.

When buying acreage, it’s essential to consider not only the interest rate but also the total monthly costs. To find out what your mortgage might cost check out this mortgage calculator.

Approval Timelines and Appraisal Challenges

Acreage properties often require more scrutiny during underwriting. When it comes to conventional vs FHA loans there are also differences in the scrutiny of appraisal for underwriting.

- FHA loans have stricter appraisal standards, which can slow timelines—especially for properties with outbuildings, mixed-use land, or unfinished infrastructure.

- Conventional loans tend to be more flexible and may close faster, particularly with lenders experienced in rural or land-based transactions.

If timing is critical, conventional financing may offer a faster process.

Flexibility for Modular and Off-Grid Builds

This is where the difference becomes most important for rural buyers. Conventional vs FHA loans may offer construction to permanent loan depending on the lender, meaning you can pay for construction on rural land.

- FHA loans can work well for modular and manufactured homes, but properties must meet specific safety and livability standards, including utilities and permanent foundations.

- Conventional loans generally offer greater flexibility for acreage, alternative building styles, and phased construction—especially when paired with construction or land-to-loan products.

For buyers planning off-grid systems, owner-built homes, or nontraditional layouts, conventional loans are often easier to navigate. It’s important to note that properties with off-grid buildings or alternative structures already on them will most likely not qualify for any loan. It is best to speak with a lender to learn what types off off-grid structures are permitted with conventional loans.

If you are interested in purchasing a property with an off-grid home already on it, you will need to get creative with owner financing or pay cash. Before getting into an owner financing situation you need to find out if the property is paid in full. If the title is not clear the loan may have a due at sale clause that requires the loan be paid in full if sold. It’s best to work with a licensed realtor or real estate attorney prior to signing any contract.

Which Loan Is Right for Buying Acreage?

- FHA loans are often best for buyers with lower credit scores, limited cash, or simple build plans.

- Conventional loans are better suited for buyers with strong credit, larger down payments, or complex rural properties.

Both options can work with conventional and FHA loans but rural land financing requires careful planning, lender selection, and an understanding of zoning, utilities, and building requirements.

👉 For a full breakdown of rural land loans, grants, USDA programs, and buyer checklists, read our complete guide: Buying Rural Land: Loans, Grants, and Programs You Need to Know.