Buying rural land is a dream for many people seeking freedom, self-sufficiency, lower costs, and a deeper connection to the land. Whether you want to build a homestead, go off-grid, raise animals, or simply escape rising housing costs, purchasing rural property is very different from buying a typical suburban home, especially if you want to finance rural land.

Financing, zoning, utilities, and regulations all work differently in rural areas—and many buyers don’t realize there are special loan programs, grants, and alternative financing options designed specifically for rural land purchases.

Before you make an offer, it’s critical to understand which financing options actually work for rural property and how lenders evaluate land differently than residential homes.

“This guide breaks down every major way to finance rural land and homestead‑ready land — from USDA and government‑backed loans to conventional and owner‑financing options — so buyers can understand their choices before committing to a property that may not qualify.”

Whether you’re planning to build, start a homestead, or simply want more space and flexibility, this guide will walk you through the financing paths that buyers commonly use — along with the limitations most people don’t discover until it’s too late.

Use the links below to jump to the sections most relevant to your situation.

- Why Buying Rural Land Is Different From Buying a Home

- USDA Rural Development Loans

- FHA & Conventional Loans for Rural Land

- Owner Financing & Private Loans

- State & Local Grants for Rural Land Buyers

- Off-Grid and Modular Build Considerations

- Affordable Land, Low Taxes, and Low Regulation

Why Buying Rural Land Is Different From Buying a Home

When you buy a house in a city or suburb, lenders focus on the structure itself. However, with rural land, lenders focus on risk.

Rural land is often considered higher risk because:

- It may not have utilities

- Access roads may be private or undeveloped

- Zoning and building rules vary widely

- Resale markets are smaller

- Income-producing uses may be restricted

Because of this, not all lenders offer rural land loans, and those that do often require higher down payments or additional documentation. That said, if you know which programs to use—and how to structure your purchase—buying rural land can be far more affordable than buying a traditional home.

USDA Rural Development Loans

One of the most powerful and underused financing tools for rural buyers is the USDA Rural Development Loan.

What Is a USDA Rural Development Loan?

USDA loans are government-backed mortgages designed to help people buy homes in eligible rural areas. These loans can finance rural land by offering:

- Zero down payment

- Lower interest rates

- Reduced mortgage insurance

- Flexible credit requirements

Despite common myths, USDA loans are not only for farmers and do not require agricultural use.

Can You Buy Rural Land With a USDA Loan?

USDA loans cannot be used to buy raw land alone, but they can be used to finance rural land and build a home by using a USDA construction-to-permanent loan. If your goal is to build a primary residence on rural land, USDA loans are often one of the most affordable paths.

USDA Loan Eligibility Basics

To finance rural land it must qualify:

- The property must be in a USDA-eligible rural area

- The home must be your primary residence

- Income must fall within limits (often higher than people expect)

- The home must meet basic safety and livability standards

To find out if a property is eligible, enter the address here.

Pros & Cons of USDA Loans

| Pros | Cons |

|---|---|

| No down payment | Cannot buy raw land |

| Lower monthly costs | Property must meet USDA standards |

| Ideal for first-time rural buyers | Income limits apply |

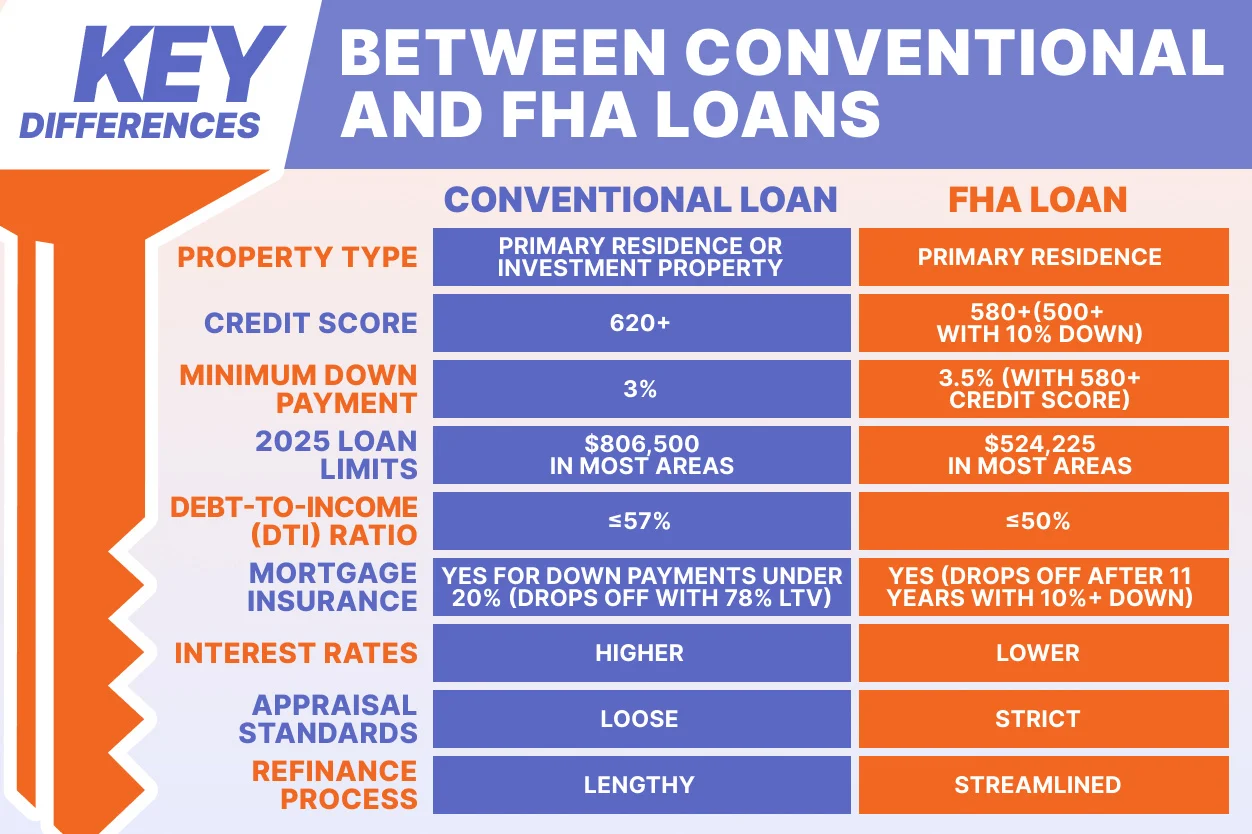

FHA & Conventional Loans for Rural Land

If USDA loans aren’t a fit, FHA and conventional financing can still work to finance rural land purchases—especially when the loan includes building a home. These loan types are most commonly used through construction-to-permanent financing, where the land purchase and home build are wrapped into a single mortgage.

FHA Loans for Rural Buyers

FHA loans are one of the most accessible options for rural buyers because they allow for low down payments and flexible credit standards. FHA financing is often used through an FHA One-Time Close Construction Loan, which combines the purchase of the land, the construction of the home, and the final mortgage into one loan.

FHA Requirements

- Minimum credit score of 580

- 3.5% down payment

- Less than 43% Debt-to-income ratio

- FHA-approved contractor

- Property must meet safety standards

Furthermore, some lenders may approve credit scores as low as 500 with a higher down payment. FHA loans also allow for higher debt-to-income ratios compared to conventional loans, making them a strong option for first-time buyers or those with limited cash reserves. Modular and manufactured homes can qualify under FHA guidelines as long as they meet HUD standards and are placed on a permanent foundation.

Calculate your Debt-to-income ratio here.

Conventional Loans for Rural Land and Acreage

Conventional loans generally have stricter requirements but offer more flexibility for higher-income buyers or larger parcels of land. Additionally, most conventional lenders require a credit score of at least 620 to 680, and when land is involved, down payments typically range from 15% to 30%, depending on whether the land is improved or raw.

Interest rates for conventional land or construction loans are usually higher than standard home loans, and lenders often require detailed building plans, contractor bids, and proof that the land is legally buildable. Therefore, conventional financing is often the best option for buyers purchasing larger acreage, raw land, or properties that fall outside FHA or USDA guidelines, especially in areas with fewer lending restrictions.

Owner Financing & Private Loans

In rural areas, owner financing is a common and often overlooked practice. Owner financing, sometimes called seller financing, bypasses the bank and allows buyers to work directly with sellers. There are several advantages to seller financing for both parties.

For example, owner financing may offer:

- Flexible terms

- Fewer lender restrictions

This can be especially useful in areas with:

- Affordable land

- Low property taxes

- Minimal zoning regulations

To find properties with owner financing, check your local Facebook groups, Craigslist, or ask a realtor who specializes in working with owner-financed properties.

Need help finding a local realtor or owner financed property? We can help.

State & Local Grants for Rural Land Buyers

Finally, many buyers assume grants don’t apply to land purchases—but that’s not true. While grants rarely cover raw land alone, many state and local programs support rural home ownership, homesteading, and land development, helping reduce the cost of buying and building on rural property.

Types of Grants & Assistance Programs

Depending on the state or region, available programs may include:

- Down payment assistance for first-time buyers

- USDA-backed home repair or improvement grants

- Infrastructure grants for wells, septic systems, electricity, and other utilities

These programs make rural property more affordable and accessible, especially for buyers building homes or improving undeveloped land.

Eligibility Requirements

Most grants have clear eligibility rules, often including:

- Income limits based on household size and local median income

- Primary residence requirement—property must be owner-occupied

- Long-term occupancy—limits resale or rental for a set period

Programs vary by state and county and are often accessed through local agencies or approved lenders. Consequently, they are typically harder to find and often won’t appear in w quick google search.

Off-Grid and Modular Build Considerations

Many rural buyers plan to live off-grid or use modular or manufactured homes. Although this can lower costs—it requires extra diligence. For instance, certain lenders will not finance rural land with off grid homes or modular homes unless they are on a foundation. This means creative financing, such as owner financing or a conventional land loan is a must.

Even if you find a property and qualify for a land loan or agree to terms with the owner you must still determine if what you want to do will be allowed on the land. This can be determined by checking zoning and land use rules through the various local county agencies.

Zoning and Land Use Rules

Above all, before buying land, verify:

- Allowed dwelling types

- Minimum square footage

- Agricultural vs residential zoning

- Restrictions on animals or outbuildings

Certainly some states and counties have very low regulatory barriers, making them popular for homesteaders and off-grid living.

Utilities, Water, and Waste

Key questions to answer before purchasing:

- First, is there a legal water source (well, spring, or shared rights)?

- Second, has the land passed a septic perc test?

- Third, will lenders require utilities to be installed?

- Lastly, are alternative systems allowed? For example composting toilet, cisterns, etc.

Water access is one of the most crucial factors in determining the value of rural land and its financing viability. Make sure you have access to water, you can look at local well logs and get an idea of how far parcels in the region are drilling before reaching water and at what gallon per minute they are providing. However, this doesn’t guarantee your land will provide the same type of well but it can give you a general idea of what to expect.

Internet, Insurance, and Access

Off grid buyers should consider these things if you plan on living full time and developing the property:

- Emergency vehicle access

- Fire protection ratings

- Internet options like satellite

- Insurance availability for rural properties

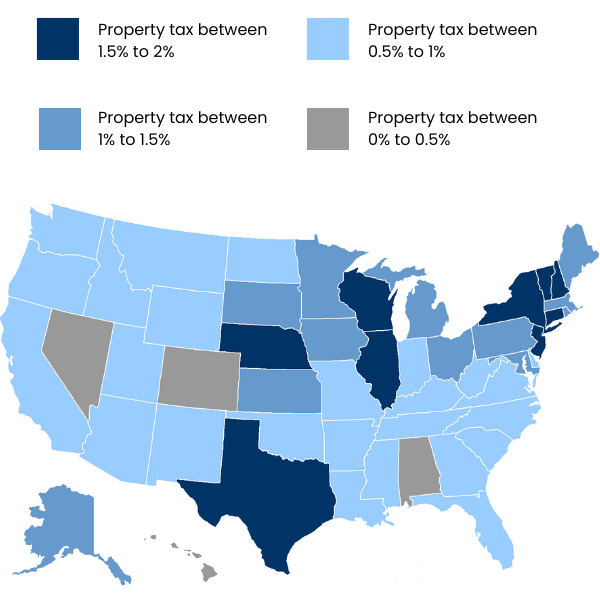

Affordable Land, Low Taxes, and Low Regulation

Additionally, other considerations include property taxes and regulations, many buyers choose rural land for financial freedom. Specifically, when determining where to build your homestead consider states with:

- Affordable land prices (New Mexico, Oklahoma, Mississippi)

- Low property taxes (Colorado, Nevada, Alabama)

- Minimal zoning and building regulations (Texas, Missouri, Arizona)

These places are especially attractive for homesteaders and self-sufficient living. These factors can dramatically impact your long-term cost of ownership.

Rural Land Buyer Checklist

Before making an offer on rural land, work through this checklist:

- Confirm zoning and allowed uses

- Verify legal road access

- Identify water source and water rights

- Check septic feasibility

- Confirm loan eligibility and whether you can finance rural land

- Review county building requirements

- Price utilities and infrastructure

- Understand long-term tax implications

Skipping any of these steps can lead to delays, financing issues, or land you can’t legally use the way you intended.

Pingback: Top 3 Things You Need To Know Before Buying Rural Land - Rooted Acres Real Estate